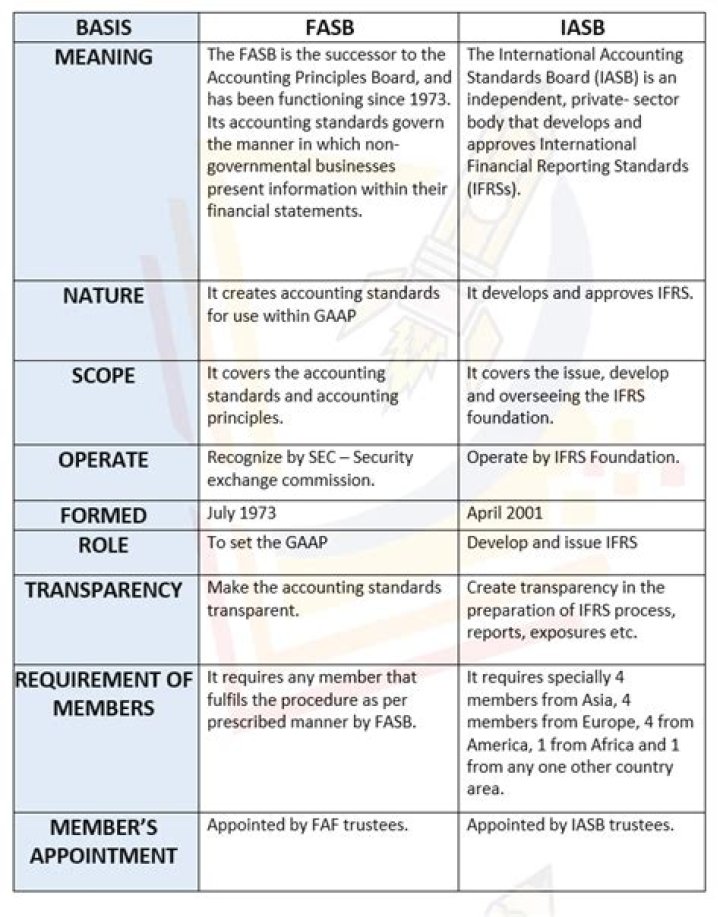

What is the difference between IFRS and IASB?

.

Similarly one may ask, what is IFRS and IASB?

International Financial Reporting Standards, commonly called IFRS, are accounting standards issued by the IFRS Foundation and the International Accounting Standards Board (IASB).

Secondly, how many IFRS standards are there? The following is the list of IFRS and IAS that issued by International Accounting Standard Board (IASB) in 2019. In 2019, there are 16 IFRS and 29 IAS.

Hereof, what IFRS means?

International Financial Reporting Standards

Why do we need IFRS?

As a source of globally comparable information, IFRS Standards are also of vital importance to regulators around the world. And IFRS Standards contribute to economic efficiency by helping investors to identify opportunities and risks across the world, thus improving capital allocation.

Related Question AnswersWhat are the main objectives of IFRS?

Its principal objectives are:- to develop, in the public interest, a single set of high quality, understandable, enforceable and globally accepted international financial reporting standards (IFRS Standards) based upon clearly articulated principles.

- to promote the use and rigorous application of those standards;

What are the advantages of IFRS?

Key benefits of IFRS. With IFRS in place, investors get greater financial and operational transparency so they can more accurately compare the health and performance of one company with that of others, and, as a result, make better fact-based investment decisions.What is IFRS and its features?

Information in IFRS financial statements has these characteristics: Relevance: So that it makes a difference to the decisions about a company made by users of the statements. Faithful representation: Financial statements are complete and free from bias and error.What is the structure of IFRS?

The IFRS Foundation has a three-tier governance structure, based on an independent standard-setting Board of experts (International Accounting Standards Board), governed and overseen by Trustees from around the world (IFRS Foundation Trustees) who in turn are accountable to a monitoring board of public authorities (Are IFRS mandatory?

IFRS Standards are required for use by all or most domestic publicly accountable entities. IFRS Standards are permitted, but not required, for use by at least some domestic publicly accountable entities, including listed companies and financial institutions.What is the function of IASB?

The IASB has overall responsibility for all technical matters, which include preparing and issuing IFRSs; preparation, and issuance, of exposure drafts; setting up procedures for reviewing comments received on documents that have been published for comment; and issuing bases for conclusions.What are the objectives of IASB?

IASB's objectives- to develop, in the public interest, a single set of high quality, understandable, enforceable and globally accepted financial reporting standards based upon clearly articulated principles.

- to promote the use and rigorous application of those standards;

Who is responsible for IFRS?

The IASB forms part of the three-tier structure employed by the IFRS Foundation and is responsible for setting the IFRS Standards and related technical activities. The IASB is overseen by the Trustees of the IFRS Foundation, responsible for the organisation's governance, the appointment of IASB members and funding.How many countries are using IFRS?

Approximately 120 nations and reporting jurisdictions permit or require IFRS for domestic listed companies, although approximately 90 countries have fully conformed with IFRS as promulgated by the IASB and include a statement acknowledging such conformity in audit reports.What is the latest IFRS standard?

This page contains links to our summaries, analysis, history and resources for: International Financial Reporting Standards. International Accounting Standards.International Financial Reporting Standards.

| # | Name | Issued |

|---|---|---|

| IFRS 14 | Regulatory Deferral Accounts | 2014 |

| IFRS 15 | Revenue from Contracts with Customers | 2014 |

| IFRS 16 | Leases | 2016 |

| IFRS 17 | Insurance Contracts | 2017 |

What is the use of IFRS in accounting?

IFRS is short for International Financial Reporting Standards. IFRS is used primarily by businesses reporting their financial results anywhere in the world except the United States. Generally Accepted Accounting Principles, or GAAP, is the accounting framework used in the United States.What is IFRS 9 in banking?

IFRS 9 is the International Accounting Standards Board's (IASB) response to the financial crisis, aimed at improving the accounting and reporting of financial assets and liabilities. IFRS 9 replaces IAS 39 with a unified standard. The classification and measurement of financial assets.What are the 4 principles of GAAP?

Basic Accounting Principles and Guidelines- Economic Entity Assumption.

- Monetary Unit Assumption.

- Time Period Assumption.

- Cost Principle.

- Full Disclosure Principle.

- Going Concern Principle.

- Matching Principle.

- Revenue Recognition Principle.

Who uses GAAP?

Generally accepted accounting principles (GAAP) are controlled by the Financial Accounting Standards Board (FASB), a nongovernmental entity. The FASB creates specific guidelines that company accountants should follow when compiling and reporting information for financial statements or auditing purposes.Why do we need IFRS in India?

As per Indian Generally Accepted Accounting Principles (I-GAAP), the revenues are computed net of excise and duties, and the current investment is valued at cost or market value. The main purpose of implementing IFRS is that it shall lower the cost of capital and bring in new opportunities.Which countries use GAAP?

This book explores differences between International Financial Reporting Standards (IFRS) and US generally accepted accounting principles (US GAAP), as well as differences in accounting practices between countries such as China, France, Germany and Japan.What are the financial statements under IFRS?

A complete set of financial statements comprises:- a statement of financial position as at the end of the period;

- a statement of profit and loss and other comprehensive income for the period.

- a statement of changes in equity for the period;

- a statement of cash flows for the period;

How many Ipsas standards are there?

38 standardsWhat are the latest accounting standards?

Applicability of Accounting standards| Accounting Standard | Level I | Level III |

|---|---|---|

| AS 3 Cash Flow Statements | Yes | No |

| AS 4 Contingencies and Events Occurring After the Balance Sheet Date | Yes | Yes |

| AS 5 Net Profit or Loss for the Period, Prior Period Items and Changes in Accounting Policies | Yes | Yes |

| AS 6 Depreciation Accounting | Yes | Yes |