What are capitalized leases

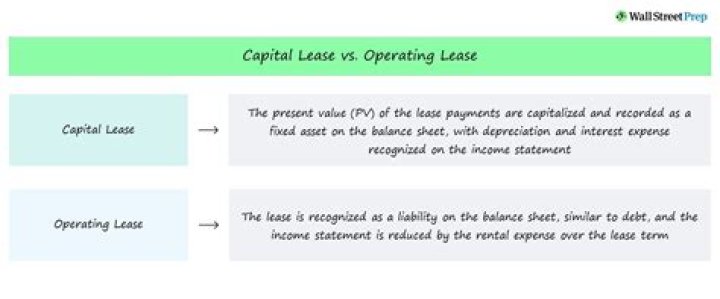

When a lease is capitalized, the lessee creates an asset account for the leased item, and the asset value on the balance sheet is the lesser of the fair market value or the present value of the lease payments. … The lessee automatically gains ownership of the asset at the end of the lease.

What are the 4 criteria for a capital lease?

- Lease Accounting. …

- Prepaid Lease.

- Fixed and Variable Costs. …

- Projecting Balance Sheet Items.

What is the purpose of a capital lease?

A capital lease is a contract entitling a renter to the temporary use of an asset and has the economic characteristics of asset ownership for accounting purposes.

What makes a lease a capital lease?

A capital lease is a lease in which the lessor only finances the leased asset, and all other rights of ownership transfer to the lessee. This results in the recordation of the asset as the lessee’s property in its general ledger, as a fixed asset.What is the difference between a capital lease and a loan?

A capital lease typically has higher monthly payments than an operating lease, is structured more like a loan, and typically has a lower residual than an operating lease. The debt and its corresponding asset, including depreciation, are shown on the balance sheet, just like a traditional loan.

Which type of lease must be capitalized?

A lessee must capitalize leased assets if the lease contract entered into satisfies at least one of the four criteria published by the Financial Accounting Standards Board (FASB). An operating lease expenses the lease payments immediately, but a capitalized lease delays recognition of the expense.

Are copier leases capital leases?

There are essentially two options available when leasing copiers: A capital lease or an operating lease. A capital lease is treated much like a loan with the equipment accounted as an asset on your balance sheet. This means that you benefit from tax depreciation and other similar benefits.

Is Rent a capital lease?

An operating lease is treated like renting — payments are considered operational expenses and the asset being leased stays off the balance sheet. In contrast, a capital lease is more like a loan; the asset is treated as being owned by the lessee so it stays on the balance sheet.Are operating leases capitalized?

Capitalizing Operating Leases The new rule, FASB ASU (Accounting Standards Update) 2016.02, will require that all leases with a term over one year must be capitalized effective for years beginning after 12/15/2021. … Operating leases will need to be recorded as equal and offsetting amounts of assets and liabilities.

Are capital leases debt?Capital leases are counted as debt. They depreciate over time and incur interest expenses. Other characteristics include: Ownership: Might transfer to the lessee at end of the lease term.

Article first time published onWhich of the following conditions would require lease capitalization?

FASB 13 (Topic 840) requires capitalizing lease payments today only if one of the following four conditions exists: The title changes hand at the end of the lease; … The lease term is > 75% of useful life of the leased assets; or. The lease payments are > 90% of the Net Present Value (NPV) of the leased assets.

What is the difference between finance and capital?

A financial account measures the increases or decreases in international ownership assets that a country is associated with, while the capital account measures the capital expenditures and overall income of a country.

Can you amortize a lease?

Amortization is the process of paying off a debt over time through regularly scheduled payments. Lease payments are amortized for the likely term of the lease by using the straight-line method.

How do you record a capital lease journal entry?

For example, if a lease payment were for a total of $1,000 and $120 of that amount were for interest expense, then the entry would be a debit of $880 to the capital lease liability account, a debit of $120 to the interest expense account, and a credit of $1,000 to the accounts payable account.

What is a single lease cost?

“A single lease cost, calculated so that the remaining cost of the lease is allocated over the remaining lease term on a straight-line basis unless another systematic and rational basis is more representative of the pattern in which benefit is expected to be derived from the right to use the underlying asset.”

How do I account for copier lease?

- Determine the amount due on the lease each month. …

- Post the balance of the lease to your “Notes Payable” account less the current month’s payment. …

- Debit the remaining amount of the lease, the current month’s payment of $1,500, to your “Office Expenses” account.

Are capital leases Current liabilities?

Current Capital Lease Obligation is the amount due within a year of balance sheet date for long-term asset lease agreements that look economically similar to asset purchases. These are listed in the liabilities section of a balance sheet.

Where is capital lease on balance sheet?

Capital leases are classified under the “fixed assets” or “plant, property and equipment” heading in the assets section of a small or large company’s balance sheet.

What does it mean to capitalize an asset?

In accounting, capitalization refers to the process of expensing the costs of attaining an asset over the life of the asset, rather than the period the expense was incurred. Rather than listing the asset as an expense, the asset is added to the company’s balance sheet and depreciated over its useful life.

How do you convert an operating lease to a capital lease?

If you want to convert an operating lease to a capital one, ask to have this option added to your terms. Calculate whether the value of the lease payments exceeds 90 percent of the value of the asset. If so, then you can treat this as a capital lease.

What is a lessor in real estate?

key takeaways. A lessor is the owner of an asset that is leased, or rented, to another party, known as the lessee. … While any sort of property can be leased, the practice is most commonly associated with residential or commercial real estate—a home or office.

Why would a company not want to capitalize a lease?

Advantage of a Capital Lease Many lessees avoid capital leases because of their balance sheet impact. When a company purchases a property, though, the acquisition cost of the property becomes an asset and any mortgage becomes a liability.

What are the 3 types of capital?

When budgeting, businesses of all kinds typically focus on three types of capital: working capital, equity capital, and debt capital.

What are the 5 sources of capital?

- Commercial Banks.

- Trade Credit.

- Equipment Suppliers.

- Savings & Loans.

- Insurance Companies.

- Credit Unions.

- Private Placements.

How is capitalization different from capital structure?

Capitalization represents permanent investment in companies excluding long-term loans. Capitalization can be distinguished from capital structure. Capital structure is a broad term and it deals with qualitative aspect of finance. While capitalization is a narrow term and it deals with the quantitative aspect.

Can rental equipment be capitalized?

View A: An entity may capitalize rental costs associated with ground and building operating leases that are incurred during the construction period. … The historical cost of acquiring an asset includes the costs necessarily incurred to bring it to the condition and location necessary for its intended use.

Is capitalized lease an intangible asset?

Although the actual property is a physical asset, the leasehold is only an interest, and therefore it is not a physical asset. A company has the contractual right to use the property for its long-term future benefit. Therefore, a leasehold meets the specifications of an intangible asset.

How should a Capitalised leased asset be depreciated by the lessee?

the depreciation policy for assets held under finance leases should be consistent with that for owned assets. If there is no reasonable certainty that the lessee will obtain ownership at the end of the lease – the asset should be depreciated over the shorter of the lease term or the life of the asset [IAS 17.27]